עקאנאמיע

#ינוועסטעו: דזשונקקער ינוועסטמענט פּלאַן אַססעססעד דורך ברועגעל טראַכטן-טאַנק נאָך ערשטער יאָר אין אָפּעראַציע

With the Juncker Plan, the European Commission intends to support valuable risky projects by expanding the risk capacity of the European Investment Bank (EIB). Grégory Claeys and Alvaro Leandro, of the Bruegel think-tank, ask if the European Fund for Strategic Investments really been used to finance 'additional' projects? The authors suggest ways in which the plan could increase its 'added value' and support more high-risk, high-return projects.

With the Juncker Plan, the European Commission intends to support valuable risky projects by expanding the risk capacity of the European Investment Bank (EIB). Grégory Claeys and Alvaro Leandro, of the Bruegel think-tank, ask if the European Fund for Strategic Investments really been used to finance 'additional' projects? The authors suggest ways in which the plan could increase its 'added value' and support more high-risk, high-return projects.

The European Commission and the EIB recently published some details about the progress of the ‘Investment plan for Europe’, after one year of its operation. The so-called Juncker plan, the European Commission’s response to the investment deficit affecting Europe since the beginning of the crisis, was officially approved in June 2015 and the European Fund for Strategic Investments (EFSI) launched immediately after. However, given the urgency of the investment situation in Europe, the pre-approval of projects had already started in April 2015 at the EIB level, in order to speed up the introduction of the plan.

What’s the plan again?

The plan’s main feature is to use a small fraction of the EU budget as a guarantee for EIB projects that would be riskier and more innovative than the usual ones. These projects would be labelled ‘EFSI projects’ and would generate a total of €315 billion of investment over the next three years through leverage and co-financing. The original idea behind the plan was to push the EIB: 1) to finance valuable riskier projects unable to secure funding today, and 2) to adopt a junior position with respect to its co-financiers to reduce the risks taken by private investors in order to increase the chances of attracting them. The resources used for the guarantee come from a reshuffling of the European Union budgets from 2015 to 2020 and are mainly taken from Horizon 2020 (ie research and innovation) and the Connecting Europe facility (ie transport infrastructure) budget lines.

Where do we stand after one year?

Since the plan got underway, €11.2bn worth of projects have been approved, initially by the EIB under the control of the Commission and, when it was finally set up at the beginning of 2016, by the EFSI Investment Committee, which is responsible for granting the support of the EU guarantee in line with the EFSI investment guidelines: €7.8bn for EFSI-labelled infrastructure and innovation projects financed by the EIB directly, and €3.4bn for SME financing through the European Investment Fund (EIF). The Juncker Plan’s take-off has been relatively slow considering that the plan foresees the EIB disbursing €60bn in three years, ie €20bn/year, which we are still quite far from for the first year. The pace needs to be accelerated if President Juncker wants to fulfil his initial promise.

Concerning EFSI investments done through the European Investment Fund (EIF), as of today they consist of 165 agreements for SME financing and take mainly the form of COSME (Competitiveness of Enterprises and SMEs) and InnovFin agreements, two EU programmes introduced in line with the new EU Multiannual Financial Framework in 2014. COSME offers both guarantees to financial institutions for them to provide financing to SMEs, and risk capital to equity funds investing in SMEs, while InnovFin offers guarantees and loans backed by Horizon 2020 funds to support research and innovation investments. The idea is therefore to use the Juncker Plan EU budget guarantee to expand these programmes. Before the adoption of the Investment Plan, the funds dedicated to these programmes in the EU budget were limited to €2.3bn over six years (2014-20) for COSME, and €2.7bn for Innovfin over the same period. Using the EU budget guarantee will therefore allow the size of these programmes to increase significantly. In theory, this seems like a good idea that could unblock investment in SMEs and in innovation projects. However, given the very recent introduction of these programmes, it is still too early to judge if this represents a good use of the EU budget guarantee.

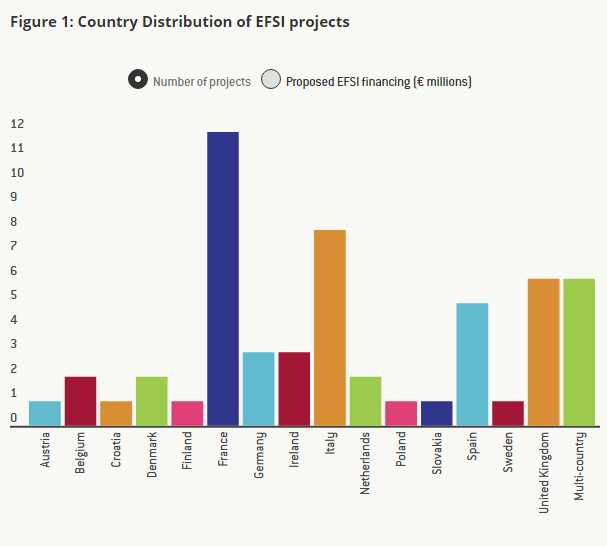

Turning to the EFSI infrastructure and innovation projects, which represent the biggest chunk of the plan, according to the Commission, 57 projects have been approved so far but details are available on the EIB website for only 55 of them.

Are EFSI projects ‘additional’?

To assess the progress of the Juncker Plan concerning infrastructure and innovation projects, let’s take a closer look at the details of each of the EFSI projects approved during its first year.

The plan will manage to successfully boost investment in Europe only if it enables valuable but risky projects currently unable to find funding. On top of that, given the opportunity costs arising from taking money from the EU’s main research and innovation (R&I) and transport infrastructure programmes, using EU budget resources to guarantee some particular EIB projects is justified only if it leads to ‘additional’ investment.

As explained in Article 5 of the EFSI regulation, projects are considered additional if they “could not have been carried out (…), or not to the same extent, by the EIB (…) without EFSI support”. Moreover, the regulation specifies that “projects supported by the EFSI shall typically have a higher risk profile than projects supported by EIB normal operations”. The best way to assess the additionality of the projects would therefore to know the risk profile of each EFSI project.

However, the information provided regarding each project is not detailed at all and generally consists of the name of the project, a short description, the amount of money invested by the EIB, the total cost of the project and some social and environmental assessment of the projects. Given the current details made available by the EIB on each project, it is not possible to directly judge their risk profile.

Nevertheless, we tried to determine using an alternative – though admittedly imperfect – method, whether these projects are ‘additional’, or at least if they are different, more innovative and riskier than the usual projects financed by the EIB, and therefore whether the diversion of EU budget funds is justified.

Using the short description and the name of each of the projects, we looked for similar projects financed by the EIB outside of the Investment Plan, and we classified them into four categories: projects for which we could find normal EIB projects with high levels of similarity, projects for which we could find EIB projects with only low levels of similarity, projects for which we could not find a similar EIB project, and projects for which not enough information is provided.

One of the Investment Plan projects is the widening of the A6 motorway between Wiesloch-Rauenberg and Weinsberg, in Germany (a total of five EFSI projects involve investment in motorways). We found a similar project which had been financed by the EIB in 2013: the widening of the A9 motorway in the Netherlands. Another example is wind farms: there are four EFSI projects involving offshore wind farms, and two onshore; meanwhile, the EIB has already funded projects involving both types of wind farms in the past (here is an example of an offshore wind farm financed by the EIB, and here is one of an onshore wind farm). Again, while it is true that projects which appear similar do not necessarily entail the same risk for the EIB, we have no information to assess this. Therefore whenever two projects involve the financing of very similar activities and there is no further information on the type of financing, then we counted them as being highly similar.

One example of an Investment Plan project for which we could only find an EIB project with ‘low’ similarity is the IMPAX Climate Property Fund II project, which involves the financing of a fund which purchases, renovates and sells commercial buildings in the UK. While we could find many EIB projects involving the rehabilitation of residential or public buildings, we could not find any involving commercial buildings. This is why we counted such projects as having ‘low’ similarity.

Out of the 55 projects approved so far for which we have details, there is only one project for which we could not find any similar EIB projects, even roughly similar: the ECOTITANIUM project, which involves the construction of the first European industrial plant to recycle and re-melt aviation-grade scrap titanium metal.

The results of our analysis can be seen in Figure 3 above: out of the 55 EFSI projects we have found very similar non-EFSI EIB projects for 42 of them; for 10 of them we found EIB projects which were somewhat similar, and for only one we could not find any similar EIB project. For one of the 55 projects, we did not have enough information to evaluate the similarity with past EIB projects.

As already mentioned, even if the projects are very similar to previous EIB projects, it is possible – and the EIB claims that this is indeed the case – that the EFSI projects are riskier, either because of the intrinsic risk of the projects, or because the EIB has a more junior position than usual, or because the maturity of the loans is much longer than usual. But the limited information currently available doesn’t allow us to verify that. However, we believe that, especially since EU budget funds are used for the Plan and that there is some opportunity cost involved in reshuffling funds from Horizon 2020 and Connection Europe facility projects to the fund guaranteeing EFSI projects, it is essential for the Commission and the EIB to demonstrate that these projects are ‘additional’ and justify benefit from the guarantee. This is particularly important because there could be incentives to give the EFSI label to projects that would have been done anyway by the EIB in the absence of the plan: for the EIB to benefit from a supplementary guarantee of their investments and for the European Commission to generate the promised €315 billion in investment through EFSI projects over three years.

According to the EFSI regulation, the EIB and the Commission are supposed to report annually to the European Parliament and the Council on the progress of the Investment Plan and on the details of the EFSI projects and in particular on their risk profile and their additionality. We urge MEPs and the EU member states to be vigilant and to hold the EIB and the Commission accountable on how these EU budget funds are used. These projects need to be particularly transparent in order to demonstrate that they are markedly riskier than the projects that the EIB would normally finance, which was the motivation for using the EU budget in the first place.

The Juncker Plan logic needs to be turned on its head

More generally, even though we are not impressed by the first year of the Juncker Plan given the current available information about the EFSI projects, we still believe that some of the ideas behind the plan can be very useful in stimulating investment in Europe through the EIB. If EFSI could result in a deep cultural change at the EIB, it would be a welcome change and could boost investment in Europe. But for that to happen, two things will have to take place.

First, EFSI should only be used for really innovative and risky projects that cannot find funding at the moment because of market failures (long term myopia of investors, too-great risk aversion on the part of private investors, underestimated cross-border positive externalities of some infrastructure investment, etc). For these projects, the EIB should also be ready to take the first losses in order to attract private investors as co-financiers.

Second, and maybe more importantly, the idea of the high multiplier is a good one but it is not used in the right place. The high ‘multiplier’ target of the Juncker plan, x15 (which can be decomposed in x3 through leverage of the EIB through debt and x5 through co-financing), was primarily designed in such a way because of the conjunction of the limited amounts of funds available for the plan and of the initial promise that was made by President Juncker in July 2014 to increase investment in Europe by €300 billion over three years.

In fact, risky and innovative EFSI projects could more easily attract private investors as co-financiers if the EIB’s share of the financing of the project was higher than it is today (or, equivalently, if the co-financing multiplier was lower). On the other hand, the EIB should finance a much smaller share of each of its usual low-risk non-EFSI projects to avoid crowding out private investors – and institutional investors in particular – especially in the current low interest rate environment. For instance, in our small sample, the EIB’s share in the total investment is 27.7% for EFSI projects vs. 48 percent for the similar non-EFSI projects. This number may not be totally representative given the small number of projects for which we have data, but it is more or less consistent with the plan in order to maximise its multiplier (x3.7 for co-financing, instead of x5). However, in the long run, this may not be the right strategy to attract private investment in risky projects.

A way to better use the EIB’s balance sheet to increase investment in Europe would be for the EIB to turn the Juncker Plan’s strategy on its head. The EIB should reduce its share in ‘traditional’ projects from between one third and one half currently to one fifth, and should act much more as a coordinator to find more co-financiers (from the private sector but also from other public development banks), while increasing the size of its tickets associated with junior positions in high-risk high-return projects. The ‘multiplier’ for the EIB’s total balance sheet would be much larger and could give a real boost to investment in Europe, even if the multiplier for EFSI itself were lower.

צו לייענען די פול אַרטיקל, גיט דאָ.

שער דעם אַרטיקל:

פראנקרייך גייט פארן נייעם אנטי-קולט געזעץ קעגן סענאט'ס אפאזיציע

נאַשאַנאַל קאָנסערוואַטיוועס וואַו צו פאָרזעצן מיט בריסל געשעעניש

NatCon ס אָנ-אַוועק זיצונג סטאַפּט דורך בריסל פּאָליצייַ

רינען: אי.יו. ינלענדיש מיניסטערס ווילן צו באַפרייַען זיך פון שמועס קאָנטראָל פאַרנעם סקאַנינג פון פּריוואַט אַרטיקלען

אי.יו. פירער פארדאמען איראן'ס 'אומגעלערטע' אטאקע אויף ישראל

NatCon זיצונג צו גיין פאָרויס אין נייַ בריסל וועניו

באָררעלל שרייבט זיין אַרבעט באַשרייַבונג

ינשורינג דעמאָקראַסי און רעספּעקט פֿאַר רעכט אין רומעניע: אַ רוף פֿאַר יוישער און אָרנטלעכקייַט

די אָסלאָ סטאַטעמענט קריייץ נייַע טשאַלאַנדזשיז פֿאַר מענטשן אַנטוויקלונג

אייראפעישער קאָונסיל אקטן אויף יראַן אָבער האפענונגען פֿאַר פּראָגרעס צו שלום

האַנדל יוניאַנז זאָגן אַז מינימום לוין דירעקטיוו איז שוין ארבעטן

פריי רייד נצחון קליימד ווי געריכט סטאַפּס סדר צו האַלטן NatCon

טורנינג הבטחות אין קאַמף: G7 ס וויטאַל ראָלע אין שטיצן די צוקונפֿט פון אוקריינא

'לאמיר נישט פארגעסן עזה' זאגט בארעל נאכדעם וואס אויסערן מיניסטערס דיסקוטירן ישראל-איראן קריזיס

NatCon ס אָנ-אַוועק זיצונג סטאַפּט דורך בריסל פּאָליצייַ

קאָמיסיע ענדאָרסיז אוקריינא פּלאַן

צוויי סעשאַנז 2024 קיקס אַוועק: דאָ ס וואָס עס איז וויכטיק

פרעזידענט שי דזשינפּינג ס 2024 ניו יאָר אָנזאָג

ינספּיראַטיאָנאַל רייַזע אַריבער טשיינאַ

א יאָרצענדלינג פון BRI: פֿון זעאונג צו פאַקט

"סניקינג קאַלץ" - אַוואַרד-ווינינג דאַקיומענטערי זיפּונג הצלחה געהאלטן אין בריסל

רעליגיע און קינדער רעכט - מיינונג פון בריסל

איבער 100 קהילה מיטגלידער געשלאגן און ערעסטיד בייַ די טערקיש גרענעץ

דיפּאַנינג ענערגיע קאָאָפּעראַטיאָן מיט אַזערביידזשאַן - אייראָפּע ס פאַרלאָזלעך פּאַרטנער פֿאַר ענערגיע זיכערהייט.

-

franceקסנומקס טעג צוריק

franceקסנומקס טעג צוריקפראנקרייך גייט פארן נייעם אנטי-קולט געזעץ קעגן סענאט'ס אפאזיציע

-

קאָנפערענסעסקסנומקס טעג צוריק

קאָנפערענסעסקסנומקס טעג צוריקנאַשאַנאַל קאָנסערוואַטיוועס וואַו צו פאָרזעצן מיט בריסל געשעעניש

-

קאָנפערענסעסקסנומקס טעג צוריק

קאָנפערענסעסקסנומקס טעג צוריקNatCon ס אָנ-אַוועק זיצונג סטאַפּט דורך בריסל פּאָליצייַ

-

מאַסע סערוויילאַנסקסנומקס טעג צוריק

מאַסע סערוויילאַנסקסנומקס טעג צוריקרינען: אי.יו. ינלענדיש מיניסטערס ווילן צו באַפרייַען זיך פון שמועס קאָנטראָל פאַרנעם סקאַנינג פון פּריוואַט אַרטיקלען